UK and European banks and EMIs: friends or foes?

Capturing the embedded finance opportunity

Electronic Money Institutions (EMIs) have played a key role in the growth of the fintech sector and are becoming systemically important. As banks look to capture embedded finance opportunities, should EMIs be viewed as competitors, collaborators, or both?

Key insights

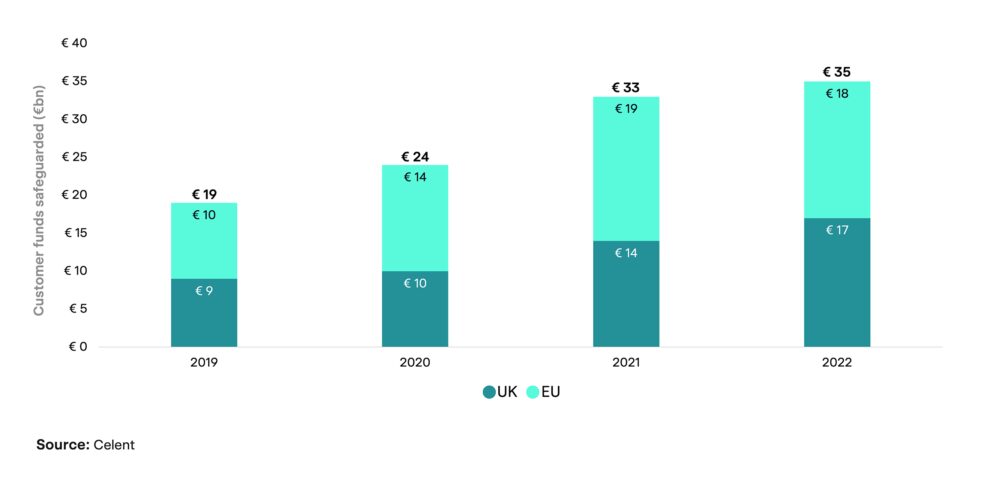

€35bn in customer funds

As the number of EMIs increases and individual EMIs grow, customer funds safeguarded by EMIs in the EU and the UK almost doubled in the last four years, standing at €35bn by the end of 2022.

Market turbulence raising regulatory scrutiny

The market has increased in size, yet it has faced several challenges in the past 18 months. Regulators are putting pressure on EMIs to demonstrate safety and resilience, while clients are increasingly concerned about long-term stability.

Safeguarding to the forefront

EMI clients are increasingly focused on how their customer funds are safeguarded, forcing firms to be more transparent over their arrangements and reevaluate their safeguarding partners.

From competitors to partners?

While it may appear that EMIs and banks can be direct competitors, the reality is more nuanced. As banks are looking to capture embedded finance opportunities, should they be viewing EMIs as competitors, collaborative partners, or perhaps both?

“This research shows how EMIs filled the gap left by incumbent banks unwilling or unable to support the fintech sector and their significant role in delivering financial services. However, recent market issues have suggested that the model has potential downsides.”

“We constantly have a debate internally to what degree our customers understand and care about FSCS protection, but we know if we could add that badge to our website, we would do it in an instant, as we think it matters.”

“Price is important, but you can always negotiate around price and try to squeeze the providers. If they don’t have the right product, technical capabilities, or don’t look safe, price becomes meaningless.”

01

EMIs in the UK and Europe

The catalyst for innovation

Electronic Money Institutions (EMIs) have played a key role in the growth of the fintech sector in Europe and are now becoming systemically important. At the end of 2022, EMIs across the UK and EU held deposits of €35bn —an increase of 84% from 2019.

The research reveals that fintech firms and EMIs are now looking to add new partners. In many cases, the intention is to enhance the product range, provide redundancies, mitigate risk and improve resilience. This evolution provides opportunities for UK and European banks and EMIs to be both competitors and partners when capturing embedded finance opportunities.

Total EMI deposits

Safeguarded customer funds in UK and Europe, 2019-2022

02

Turbulence in the sector

Driving increased regulatory scrutiny

Recent market issues have brought the issues of safety and operational resilience to the top of the agenda. An increasing regulatory focus is understandable: the financial ecosystem has become increasingly open and interconnected, and problems in a single supplier can ripple through multiple other providers.

As a result, regulators are putting a renewed emphasis on ensuring that all market participants have robust operational resiliency, fraud and AML controls and safeguarding of customer funds. Likewise, participants across the industry are evaluating whether their networks of partners and service providers have the necessary stability and resilience to survive this period of turbulence.

03

Partner considerations

The evolving selection criteria

The research found a clear hierarchy of requirements where product and risk appetite alignment dominate partner selection criteria. For example, some banks and even EMIs have clear rules against supporting firms in certain industries, such as gambling or crypto.

Safeguarding is another critical aspect. Firms are paying closer attention to safeguarding practices during due diligence, seeking to better understand an EMIs approach. That, in turn, is forcing EMIs to improve their practices and reconsider their safeguarding partners.

Other key considerations include technical capabilities and breadth of functionality, with ease of integration and quality of APIs at the top of the list of requirements.

Download your copy now

UK and European banks and EMIs: friends or foes?

Experience the ClearBank difference and begin your journey today.