Digital assets, tokenisation and the future of payments

The shift from cash to assets is a natural progression, driven along the way by the increasing digitisation of financial transactions. As more people accept digital assets as a payment method and use them as a store of value, individuals and businesses alike unlock the advantages of a digital economy in the form of faster and lower transaction costs, greater transparency and enhanced convenience.

State Street’s recent report on tokenisation and digital asset regulation highlights their potential, emphasising the need for frameworks that strike a balance between encouraging innovation and safeguarding investor protection. Furthermore, it underscores that a regulated environment can unlock the potential of digital assets by offering a secure and transparent platform for their issuance, trading and use.

Digital assets (as a form of payment) are simply an alternative way to pay for goods and services and do not need to mean that cash is no longer available for those who still wish to transact with it. Tokenising and creating digital assets backed by real world assets, such as real estate and securities, improve liquidity and accessibility and the added transparency helps to build trust whilst giving governments another tool with which to help meet the challenges of the shadow economy.

With the changing landscape, traditional financial institutions such as banks, card networks and even global payments network SWIFT are finding themselves compelled to adapt. They are recognising the potential of the emerging asset ecosystem, looking for ways to offer alternative payment options and tap into new market segments. Whether it is through partnerships, investments or developing their own asset solutions, these banks and network providers are poised to play a crucial role in shaping the future of money.

Although cryptocurrencies have captured considerable focus, the notion of tokenisation reaches well beyond digital money; it transforms the way assets are depicted and exchanged, improving security, effectiveness and usability across diverse sectors.

Major players in the industry, such as Visa, Mastercard, Google Pay and Apple Pay, use tokenisation extensively to reinforce security within financial transaction systems.

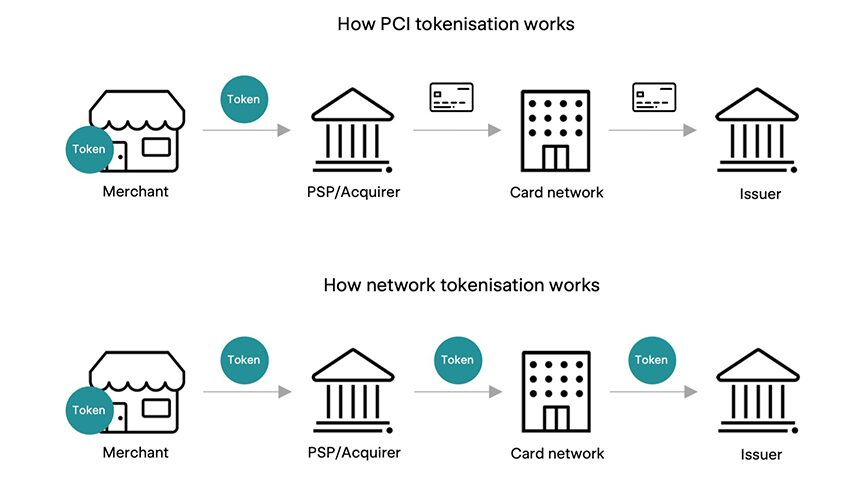

In brief, tokenisation is the process of converting real-world assets such as stocks, real estate or even intellectual property into digital tokens that are recorded on a blockchain. These blockchain tokens are backed by the assets themselves and come with identifiers, ensuring high levels of security and protection against tampering. By utilising certain techniques, tokenisation effectively reduces the risk of fraud and counterfeiting, creating a trustworthy environment for transactions.

The success of tokenisation can be seen in networks such as Visa and Mastercard, which have incorporated this approach to enhance the security of card transactions. In card payments, sensitive card information is stored in merchant systems, which makes them vulnerable to data breaches. However, tokenisation replaces this information with tokens during transactions so ensuring that actual card details are never shared, and this significantly decreases the likelihood of data theft or unauthorised transactions.

Visa recently announced that it has issued over 4 billion tokens, emphasising that they are useless to cybercriminals without the corresponding encryption keys. This robust security provided by tokenisation has also led to improved approval rates for both consumers and merchants:

"Visa analysis shows that across more than 8,600 issuers and 800,000 merchants, Visa tokens have led to a 28 percent reduction in fraud rates and a 3 percent increase in approval rates - increasing sales for merchants while saving them money on fraud-related expenses."

Furthermore, tokenisation is proving its effectiveness in ensuring transactions - its usage is now extending beyond just simply payment systems, paving the way for an era of ownership and exchange. Meanwhile, Mastercard has introduced the Multi Token Network (MTN) program with the aim of enhancing security, efficiency and scalability in asset transactions by focusing on four trust-based goals:

- Trust in the counterparty: Mastercard is working to create common standards and infrastructure for verifying identities and permissions on blockchain networks. This will help consumers and businesses interact with confidence.

- Secure digital payments: Mastercard has already experimented with tokens representing deposits at commercial banks, and the MTN will continue to support these efforts to create stable, regulated and scalable blockchain tokens for payment applications.

- Technology resilience: improving the ability of blockchain networks to handle large numbers of transactions and interact with each other effectively. Mastercard has been working with the Reserve Bank of Australia and other partners on a pilot program that shows how this can be done, and the MTN will aim to offer these capabilities more broadly.

- Prioritising consumer protection: using Mastercard’s experience in setting standards and rules for its card network to create a framework that prioritises consumer protection, stability and regulatory compliance.

In addition, Mastercard has spent over $3.21 billion on 19 acquisitions and 72 investments as it builds out its digital asset infrastructure across multiple sectors such as payments, cybersecurity and regtech, including:

- Ciphertrace (September 2021) - providing digital asset monitoring and analysis to aid fraud detection and prevention.

- Ekata (June 2021) - specialising in digital identity verification.

- nudata Security (March 2017) - helping identify authentic users through behavioural biometric indicators when clients spend online.

- RiskRecon (December 2017) - providing enterprise risk management and security services.

The evolution of money and, therefore, payments point toward a diverse future.

The rise of digital assets, including cryptocurrencies and central bank digital currencies (CBDCs) is challenging traditional payment systems and reshaping the financial landscape. Tokenisation, the creation of digital tokens backed by real-world assets, will provide a method for enhancing the accessibility and transparency of those assets.

As we observe this transformative change, a few questions come to mind. How will financial institutions seize the opportunities presented? And how will they navigate the upcoming challenges in shaping a future where digital assets offer the potential to become units of exchange and stores of value? While some of this will likely be answered by digital asset regulation that looks to balance innovation and consumer protection, financial institutions and network providers will also need redefine their roles in the future.

Discover how ClearBank is supporting digital asset firms with innovative payment services here.

Sukhy Atwal is Head of Wealth, Pensions and Insurance at ClearBank